Gold’s price has been on the rise since our last report proving that the halt of its drop was a reversal of direction and not a mere stabilisation. On a fundamental level we note the following:

- Gold’s price has been consistently rising over the past week while at the same time we note that the USD has been falling. The two trading instruments over the past week have displayed in the big picture that their negative correlation has been in effect. Thus should we see the USD weakening further, we may see at the same time gold’s price gaining and vice versa. On the other hand US yields, despite some ups and downs, remained relatively stable, unable to materially affect gold’s price. Yet should we see US yields consistently rise over the coming week, we may see gold’s price retreating as US bonds may start posing a more attractive alternative for safe haven investment than gold, given that the precious metal is not only not bearing any interest but also has storage costs. One scenario that could cancel such a scenario would be that US bond yields rise given that market worries are related to the macroeconomic outlook of the US, thus rendering the possible attractiveness of US bonds as useless.

- In the coming week, we note two US financial releases that could affect also gold’s price. The first would be the revised US GDP rate for Q1 and any acceleration of the GDP rates could support gold’s price as it could ease market worries for the US economic outlook. The second release would be on Friday, the PCE rates for April, which is also the Fed’s favorite inflation metric. Should the rates accelerate or in general show a relative persistence of inflationary pressures we may see more pressure being exercised on the Fed to keep rates high for longer thus weighing on gold’s price.

- For the time being we note that Fed policymakers seem to maintain their doubts about the necessity of lowering rates quickly which in turn tends to be clipping any gains for gold’s price. For the time being the markets’ expectations are for only rate cut and that to be delivered in the December meeting, signalling that he market may have allready substantially eased its dovish expectations, with little room for further retreats.

- Last but not least we note that US President Trump has postponed another 50% tariff on European products entering US soil, which was announced only on Friday. The postponement runs until the 9th of July. The overall issue tended to provide safe haven inflows for gold’s price on Friday, as markets were caught by surprise. The overall issue tends to highlight the uncertainty surrounding US President Trump’s intentions which tends to maintain a nervousness in the markets which in turn affects gold’s price. Should we see more negative surprises emerging from US President Trump, we may see gold’s price getting support and vice versa.

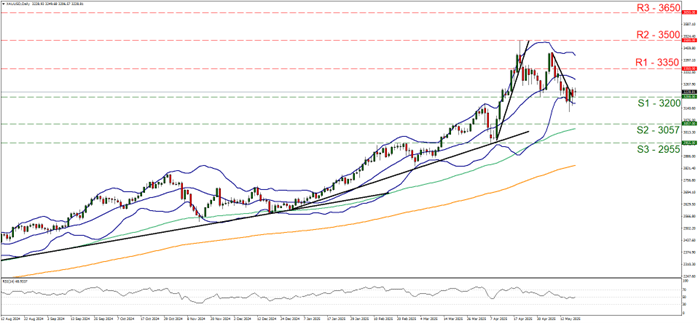

Technical analysis

Gold’s price edged higher on Friday forcing us to re-adjust the R1 level at $3366/troy ounce. Given the upward motion of the precious metal’s price we tend to maintain a bullish outlook, as long as the upward trendline incepted since the 15th of May remains intact. On the other hand, we have to note that the RSI indicator is not so encouraging for gold bulls as it remains close to the reading of 50 despite edging higher and the Bollinger bands remain flat with a relatively steady width. Both indicators tend to point towards a possible sideways motion of gold’s price, yet withing wide bands.

Should the bulls maintain control as expected we may see gold’s price breaking above the 3366 (R1) resistance line clearly, thus paving the way for the 3500 (R2) resistance level. For a bearish outlook would require gold’s price to initially break the prementioned upward trendline, in a first signal that the upward motion has been interrupted and continue lower to break the 3200 (S1) support line clearly, practically opening the gates for the 3057 (R2) support base.

- Support: 3200 (S1), 3057 (S2), 2955 (S3)

- Resistance: 3366 (R1), 3500 (R2), 3650 (R3)