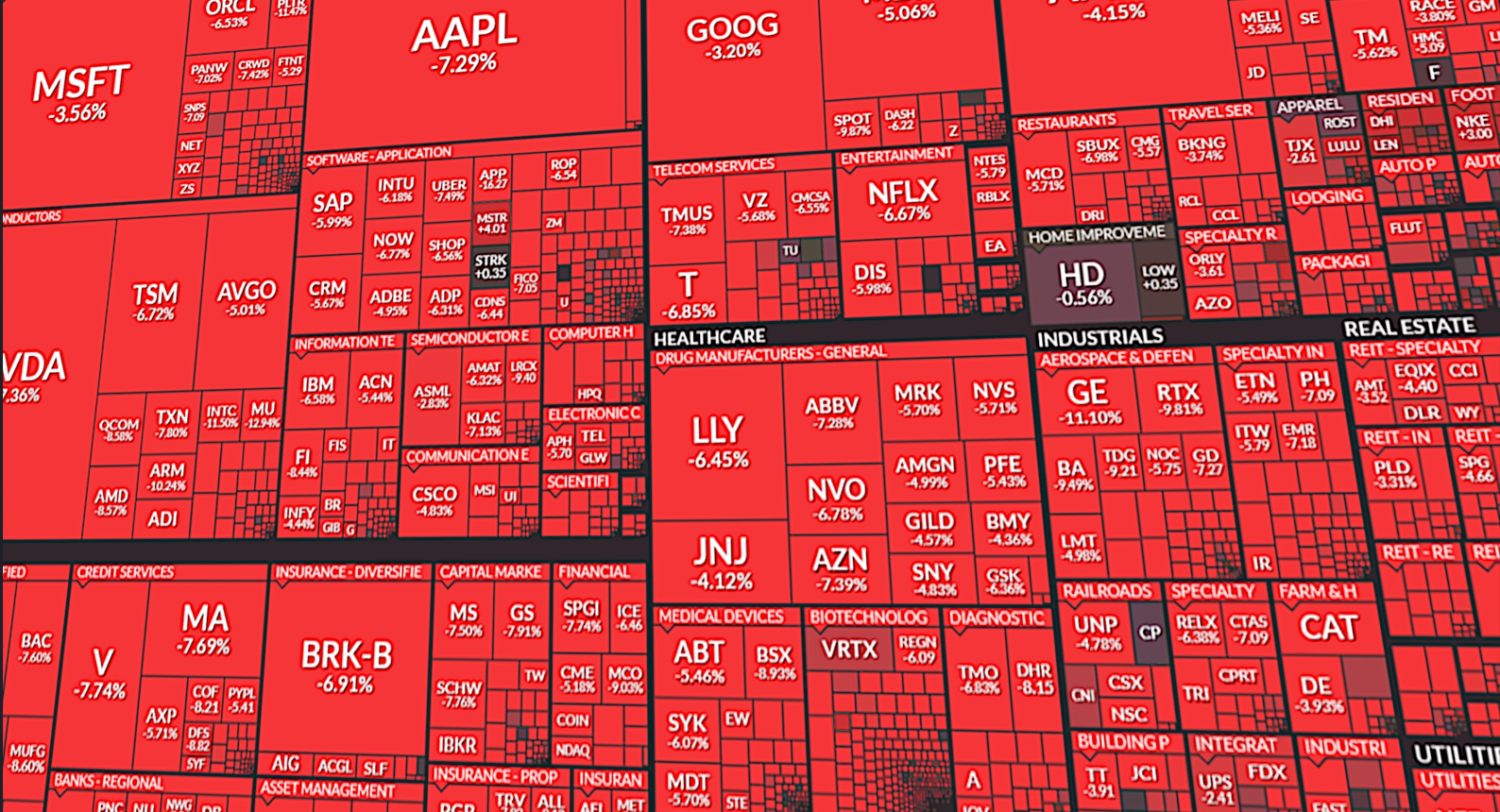

Given the lack of economic news releases today Monday, we decided to outline the most important and crucial events scattered across this week on the economic, policy and earnings fronts:

Tuesday: We begin with the BoJ Core CPI print in the early Asian session and the CB consumer confidence indicator for the month of October from the United States. On the earnings front we note the releases from Visa, UnitedHealth, HSBC, Novartis and Booking.com.

Wednesday: We note Australia’s quarterly CPI update in the Asian session, the Bank of Canada’s monetary policy decision alongside the most important event of the week, the Federal Reserve’s interest rate decision for the meeting of October, alongside the speech from Fed Chair Powell. On the earnings front we underscore the releases from most of the magnificent seven heavyweights, namely Microsoft, Alphabet and Meta, but announcements Boeing, Caterpillar, Verizon and ServiceNow as well.

Thursday: In another data packed day, we note the Bank of Japan’s policy rate decision early on, preliminary third quarter GDP updates from Germany, France, Eurozone as a whole and the United States, but more importantly the European Central Bank’s interest rate decision of the October meeting alongside the speech from President Lagarde. As for earnings, tech behemoths Apple and Amazon report in the aftermarket hours, alongside Eli Lilly, Mastercard, Shell and Merck.

Friday: We close the show with Tokyo’s Core CPI, manufacturing and services PMI updates from China, the preliminary HICP update from Eurozone and finally from the US, we note update of the Fed’s favourite inflation metric, the Core PCE index. On the earnings front we note Q3 releases from ExxonMobil, Chevron, AbbVie and Intesa Sanpaolo.

Technical Analysis

XAUUSD Chart – Gold outflows intensify as markets remain hopeful of a US-China trade deal

Resistance: 4150 (R1), 4250 (R2), 4380 (R3)

Support: 4000 (S1), 3890 (S2), 3780 (S3)